August 27, 2025, Sudbury, Ontario – Magna Mining Inc. (TSXV: NICU) (OTCQX: MGMNF) (FSE:8YD) (the “Company” or “Magna”) is pleased to report second quarter 2025 operating and financial results. Management will host a conference call tomorrow, August 28, 2025, at 08:00 a.m. EDT to discuss the results. All amounts are expressed in Canadian dollars unless otherwise indicated.

Highlights

- April-June 2025 (“Q2”) was the first full quarter of production from the McCreedy West copper mine under Magna’s operation.

- Total ore processed in Q2 was 59,100 tons from the 700 Footwall Copper Zone and 10,945 tons from the Intermain Nickel Zone, for a combined total of 70,045 tons.

- Combined ore grade for the quarter was 3.26% Copper Equivalent (“Cu Eq”).

- End of period cash balance of $27 million.

Jason Jessup, CEO, commented “Since we acquired the McCreedy West Mine on February 28, 2025, we have implemented multiple mine optimization initiatives and invested substantial capital in equipment and underground development to improve the operation. During the quarter we increased our staff and workforce, made management changes and realized a material increase in the amount of daily development completed at the mine. Throughout Q2, we started to see evidence of these operational improvements, with month over month increases in the amount of payable copper-equivalent pounds as well as improved grades produced at the operation. More importantly, we are consistently improving on the productivity of our development crews, which will lead to more workplaces in the mine and better flexibility in our mine plan. The second quarter, and the remainder of 2025, is focused ensuring the mine is in a strong position for 2026 production. I am pleased with the results to date and look forward to building this operation into a long-life, sustainable producer that generates free cash flow.”

Table 1: Magna Mining Q2 2025 Tons Mines, Payable Copper Equivalent Pounds and Grades

1 Copper equivalent payable pounds and copper equivalent payable grade were calculated using the following US dollar prices:

Q2 2025: $4.29/lb Cu, $6.88/lb Ni, $15.81/lb Co, $1,072.35/oz Pt, $990.29/oz Pd, $3,301.29/oz Au, $33.64 Ag.

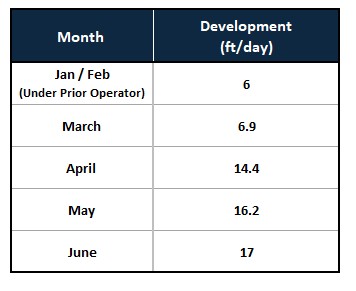

Table 2: McCreedy West Q1 and Q2 2025 Development Rates

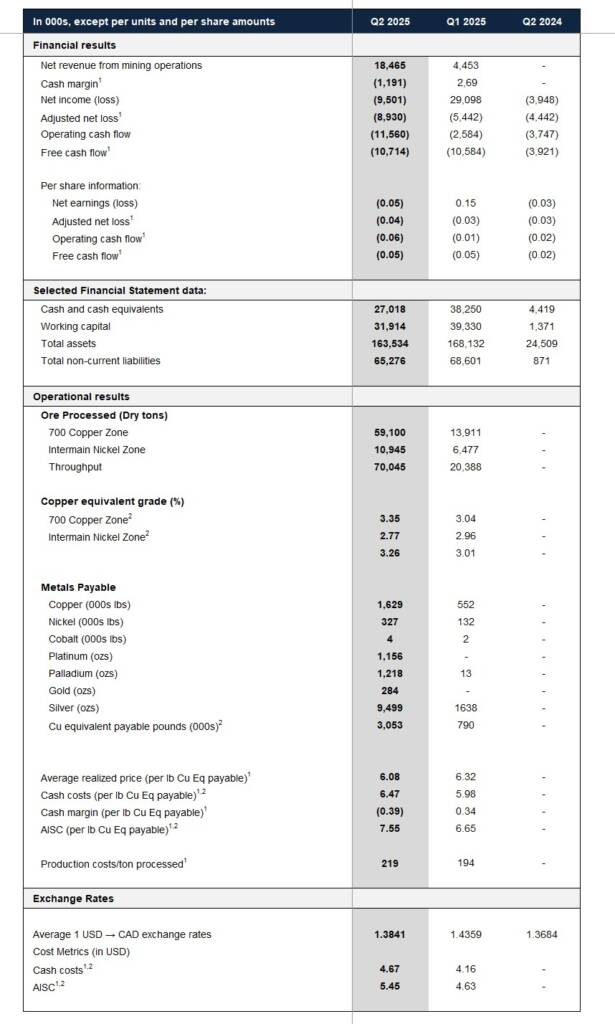

Table 3: Q2 2025 Operating and Financial Highlights

1 For the reconciliation of these non-IFRS measures to the consolidated financial statements, please see the reconciliations at the end of this news release. Magna uses non-IFRS performance measures in this news release as it believes that these generally accepted industry performance measures provide a useful indication of the Company’s operational performance. Non-IFRS performance measures do not have standardized meanings defined by IFRS Accounting Standards and may not be comparable to information in other issuers’ reports and filings. They should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS Accounting Standards.

2 Copper equivalent payable pounds for the purpose of copper equivalent payable grade, cash cost and AISC were calculated using the following US dollar prices:

Q2 2025: $4.29/lb Cu, $6.88/lb Ni, $15.81/lb Co, $1,072.35/oz Pt, $990.29/oz Pd, $3,301.29/oz Au, $33.64 Ag.

Q1 2025: $4.40/lb Cu, $7.18/lb Ni, $15.38/lb Co, $944.31/oz Pt, $1,005.61/oz Pd, $3,135.60/oz Au, $34.61 Ag.

Q2 Financial Highlights

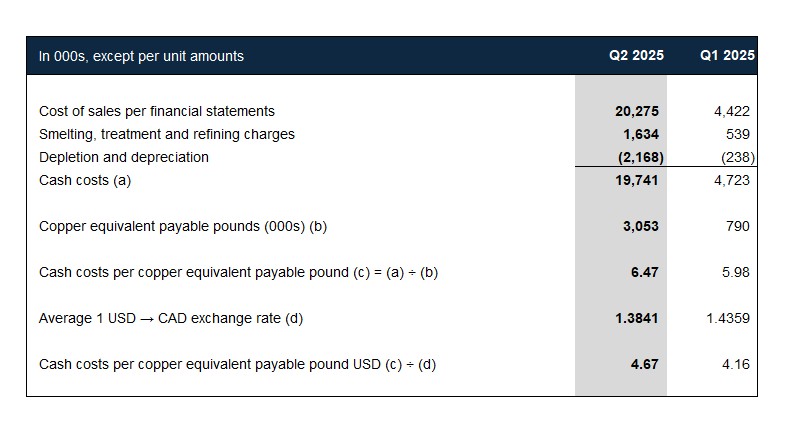

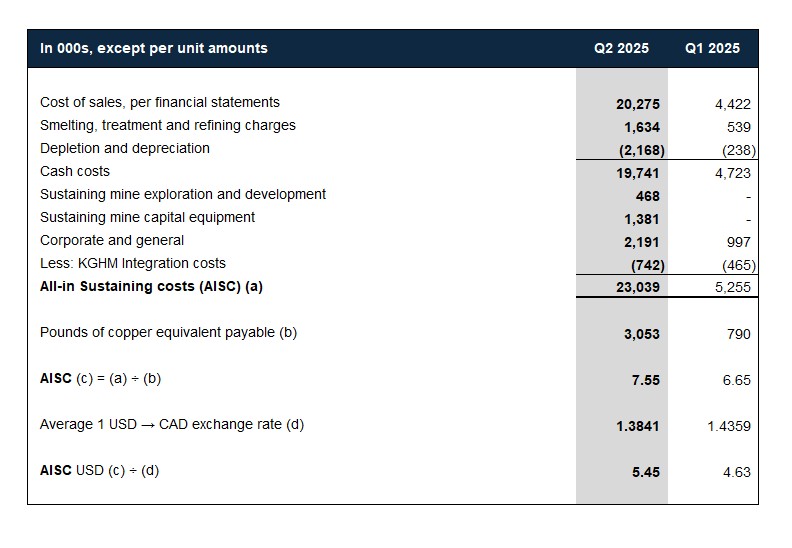

- Q2 cash costs were C$6.47 per pound or US$4.67.

- All in sustaining costs for the same quarter were C$7.55 per pound or US$5.45, which includes the purchase of a scoop tram, and developing 282 equivalent feet of capital development.

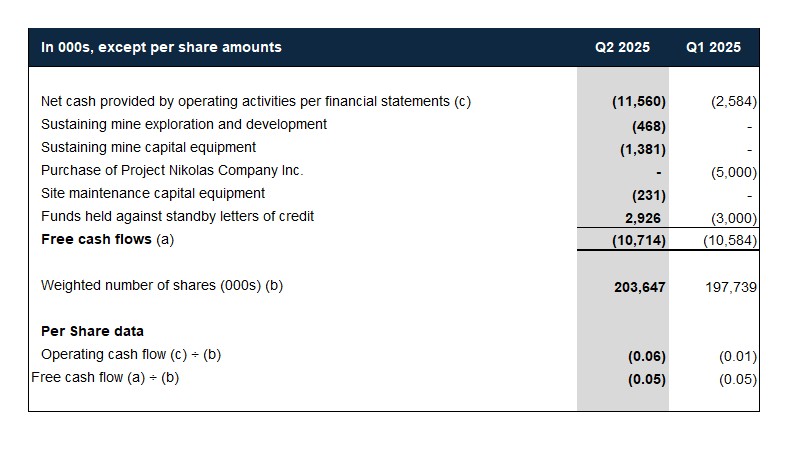

- Operating cash outflow of $11.6 million.

- Free cash outflow of $10.7 million.

- Adjusted net loss of $8.9 million.

- End of period cash balance of $27 million.

Further details regarding the calculation of production costs, cash margins and all in sustaining costs can be found in the quarterly MD&A.

Q2 Operational Highlights

- McCreedy West produced 3.05 million pounds of copper equivalent payable in the quarter at an average grade of 3.26% Cu Eq.

- Total ore processed in Q2 was 59,100 tons from the 700 Footwall Copper Zone and 10,945 tons from the Intermain Nickel Zone.

- April production was affected by a lack of operating and capital development completed in the preceding quarters while the mine was under prior ownership (Table 1 and Table 2). Production in April also included tonnage from the Intermain Nickel Zone that was previously developed by the prior operators.

- Underground development increased from 14.4 feet per day in April to 17.0 feet per day in June.

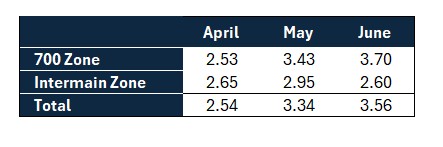

Table 4: McCreedy West Q2 2025 Cu Eq Contained Grade (%) By Zone

Webcast Link

Webcast Link: https://www.gowebcasting.com/14155

Participant Dial In: (N. America Toll Free): 1-844-763-8274

Participant International Dial In: 1-647-484-8814

Conference call participants should ask to join the Magna Mining Inc. quarterly results conference call.

Qualified Person

The scientific or technical information in this press release has been reviewed and approved by David King, M.Sc., P.Geo. Mr. King is the Senior Vice President, Exploration and Geoscience for Magna Mining Inc. and is a qualified person under Canadian National Instrument 43-101.

Cautionary Note Regarding Forward-Looking Statements

All statements, other than statements of historical fact, contained or incorporated by reference in this press release constitute “forward-looking statements” and “forward-looking information” (collectively, “forward-looking statements”) within the meaning of applicable securities laws. Generally, these forward-looking statements can be identified by the use of forward-looking terminology, such as “may”, “might”, “potential”, “expect”, “anticipate”, “estimate”, “believe”, “could”, “should”, “would”, “will”, “intend”, “plan”, “forecast”, “prospective”, “significant” or other similar words or phrases or variations thereof. Forward-looking statements are necessarily based upon a number of assumptions that, while considered reasonable by management, are inherently subject to business, market and economic risks, uncertainties and contingencies that may cause actual results, performance or achievements to be materially different from those expressed or implied by forward-looking statements, including risks relating to the failure to realize anticipated or assumed production and operational improvements from current or planned optimization initiatives at the McCreedy West mine, the failure to commence or complete as quickly as planned additional development work at McCreedy West, the failure to successfully realize on talent and technical expertise to unlock the long-term, sustainable potential of McCreedy West or other assets of the Company and other risks disclosed in the Company’s most recent annual management discussion and analysis, available on the SEDAR+ website (at: www.sedarplus.ca). Although the Company has attempted to identify important risks, uncertainties, contingencies and factors that could cause actual results to differ materially from those expressed or implied in forward-looking statements, there can be no certainty or assurance that the Company has accurately or adequately captured, accounted for or disclosed all such risks, uncertainties, contingencies or factors. Readers should place no reliance on forward-looking statements as actual results, performance or achievements may be materially different from those expressed or implied by such statements. Resource exploration and development, and mining operations, are highly speculative, characterized by several significant risks, which even a combination of careful evaluation, experience and knowledge will not eliminate. Forward-looking statements speak only as of the date they are made. The Company does not undertake to update any forward-looking statements, whether as a result of new information or future events or otherwise, except in accordance with applicable securities laws.

About Magna Mining Inc.

Magna Mining Inc. is a producing mining company with a strong portfolio of copper, nickel, and platinum group metals (PGM) assets located in the world-class Sudbury mining district of Ontario, Canada. The Company’s primary asset is the McCreedy West Mine, currently in production, supported by a pipeline of highly prospective past-producing properties including Levack, Crean Hill, Podolsky, and Shakespeare.

Magna Mining is strategically positioned to unlock long-term shareholder value through continued production, exploration upside, and near-term development opportunities across its asset base.

Additional corporate and project information is available at www.magnamining.com and through the Company’s public filings on the SEDAR+ website at www.sedarplus.ca.

For further information, please contact:

Jason Jessup

Chief Executive Officer

or

Paul Fowler, CFA

Senior Vice President

705-482-9667

Email: info@magnamining.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accept responsibility for the adequacy or accuracy of this press release.

NON-IFRS PERFORMANCE MEASURES

Please see below for the reconciliation of non-IFRS measures referred to in this news release to the consolidated financial statements.

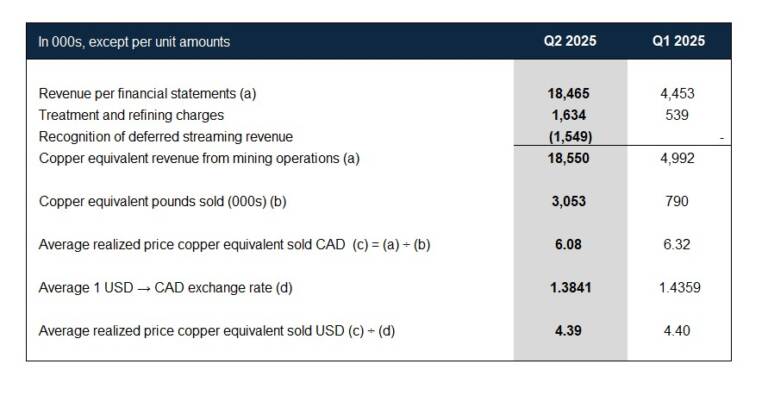

Average realized price per copper equivalent payable pound

Average realized price per copper equivalent payable pound is a non-IFRS Accounting Standards measure and does not constitute a measure recognized by IFRS Accounting Standards and does not have a standardized meaning defined by IFRS Accounting Standards. Average realized price per copper equivalent payable pound is calculated by dividing total metal proceeds received by the Company for the relevant period by the copper equivalent payable pounds. It may not be comparable to information in other issuers’ reports and filings.

Cash costs per copper equivalent payable pound

Cash cost per copper equivalent payable pound is a non-IFRS Accounting Standards performance measure and does not constitute a measure recognized by IFRS Accounting Standards and does not have a standardized meaning defined by IFRS Accounting Standards, as well it may not be comparable to information in other issuers’ reports and filings. The Company has included this non-IFRS Accounting Standards performance measure throughout this document as Magna believes that this generally accepted industry performance measure provides a useful indication of the Company’s operational performance. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance and ability to generate cash flow. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. The following table provides a reconciliation of total cash costs per copper equivalent payable pound to cost of sales per the financial statements for each of the last eight quarters:

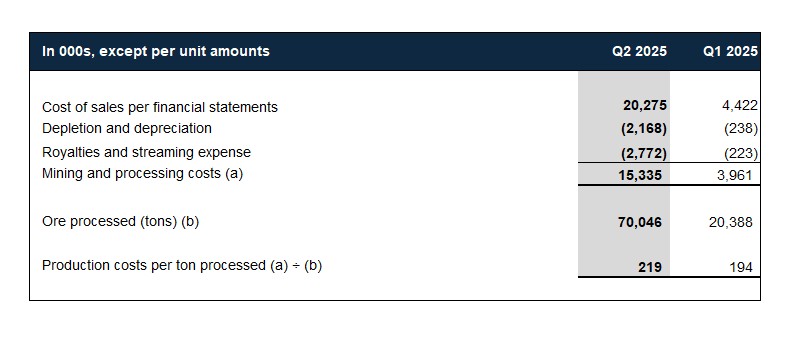

Production costs per ton processed

Mine-site cost per ton processed is a non-IFRS Accounting Standards performance measure and does not constitute a measure recognized by IFRS Accounting Standards and does not have a standardized meaning defined by IFRS Accounting Standards, as well it may not be comparable to information in other issuers’ reports and filings. As illustrated in the table below, this measure is calculated by adjusting cost of sales, as shown in the statements of income for non-cash depletion and depreciation, royalties and inventory level changes and then dividing by tons processed through the smelter. Management believes that mine-site cost per ton processed provides additional information regarding the performance of mining operations and allows Management to monitor operating costs on a more consistent basis as the per ton processed measure reduces the cost variability associated with varying production levels. Management also uses this measure to determine the economic viability of mining blocks. As each mining block is evaluated based on the net realizable value of each ton mined, the estimated revenue on a per ton basis must be in excess of the production cost per ton processed in order to be economically viable. Management is aware that this per ton processed measure is impacted by fluctuations in throughput and thus uses this evaluation tool in conjunction with production costs prepared in accordance with IFRS Accounting Standards. This measure supplements production cost information prepared in accordance with IFRS Accounting Standards and allows investors to distinguish between changes in production costs resulting from changes in production versus changes in operating performance.

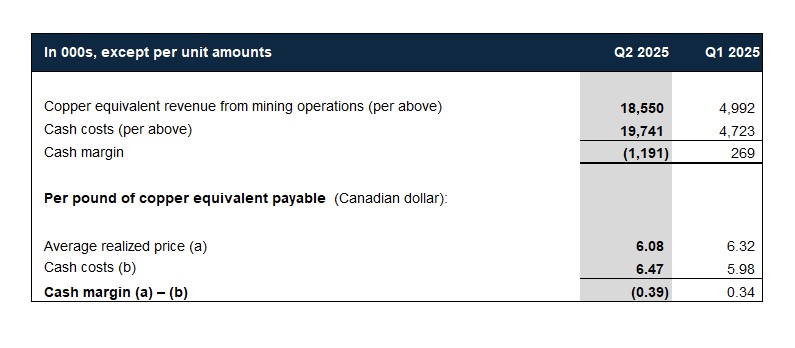

Cash Margin

Cash margin is a non-IFRS Accounting Standards measure and does not constitute a measure recognized by IFRS Accounting Standards and does not have a standardized meaning defined by IFRS Accounting Standards, as well it may not be comparable to information in other issuers’ reports and filings. It is calculated as the difference between total sales revenue, net of smelting, refining and treatment costs from mining operations and cash mine site operating costs (see Cash cost per ounce of gold sold under this Section above) per the Company’s Financial Statements. The Company believes it illustrates the performance of the Company’s operating mines and enables investors to better understand the Company’s performance in comparison to other metal producers who present results on a similar basis.

All-in Sustaining Costs

All-in sustaining costs (“AISC”) include mine site operating costs incurred at Magna mining operations, sustaining mine capital and development expenditures, mine site exploration expenditures and equipment lease payments related to the mine operations and corporate administration expenses. The Company believes that this measure represents the total costs of producing copper equivalent payable pounds from current operations and provides Magna and other stakeholders with additional information that illustrates the Company’s operational performance and ability to generate cash flow. This cost measure seeks to reflect the full cost of copper production from current operations on a per-pound basis of copper equivalent payable. New project and growth capital are not included.

Free Cash Flow and Operating and Free Cash Flow per Share

Free cash flow is calculated by taking net cash provided by operating activities less cash used in capital expenditures and lease payments as reported in the Company’s financial statements. Free cash flow per share is calculated by dividing free cash flow by the weighted average number of shares outstanding for the period.

Operating cash flow per share is a non-IFRS Accounting Standards measure and does not constitute a measure recognized by IFRS Accounting Standards and does not have a standardized meaning defined by IFRS Accounting Standards. Operating cash flow per share is calculated by dividing cash flow from operating activities in the Company’s Financial Statements by the weighted average number of shares outstanding for each year. It may not be comparable to information in other issuers’ reports and filings.

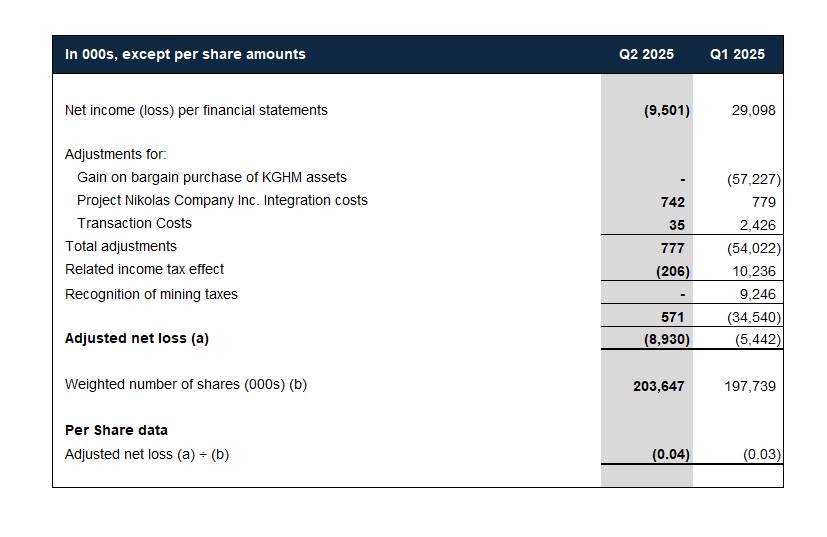

Adjusted Net Loss and Adjusted Net Loss per Share

Adjusted net loss and adjusted net loss per share are non-IFRS Accounting Standards performance measures and do not constitute a measure recognized by IFRS Accounting Standards and do not have standardized meanings defined by IFRS Accounting Standards, as well both measures may not be comparable to information in other issuers’ reports and filings. Adjusted net loss is calculated by removing the one-time gains and losses resulting from the disposition of non-core assets, non-recurring expenses and significant tax adjustments (mining tax recognition and exploration credit refunds) not related to current period’s income, as detailed in the table below. Magna discloses this measure, which is based on its financial statements, to assist in the understanding of the Company’s operating results and financial position.